{kind=link}

Image source: Getty Images

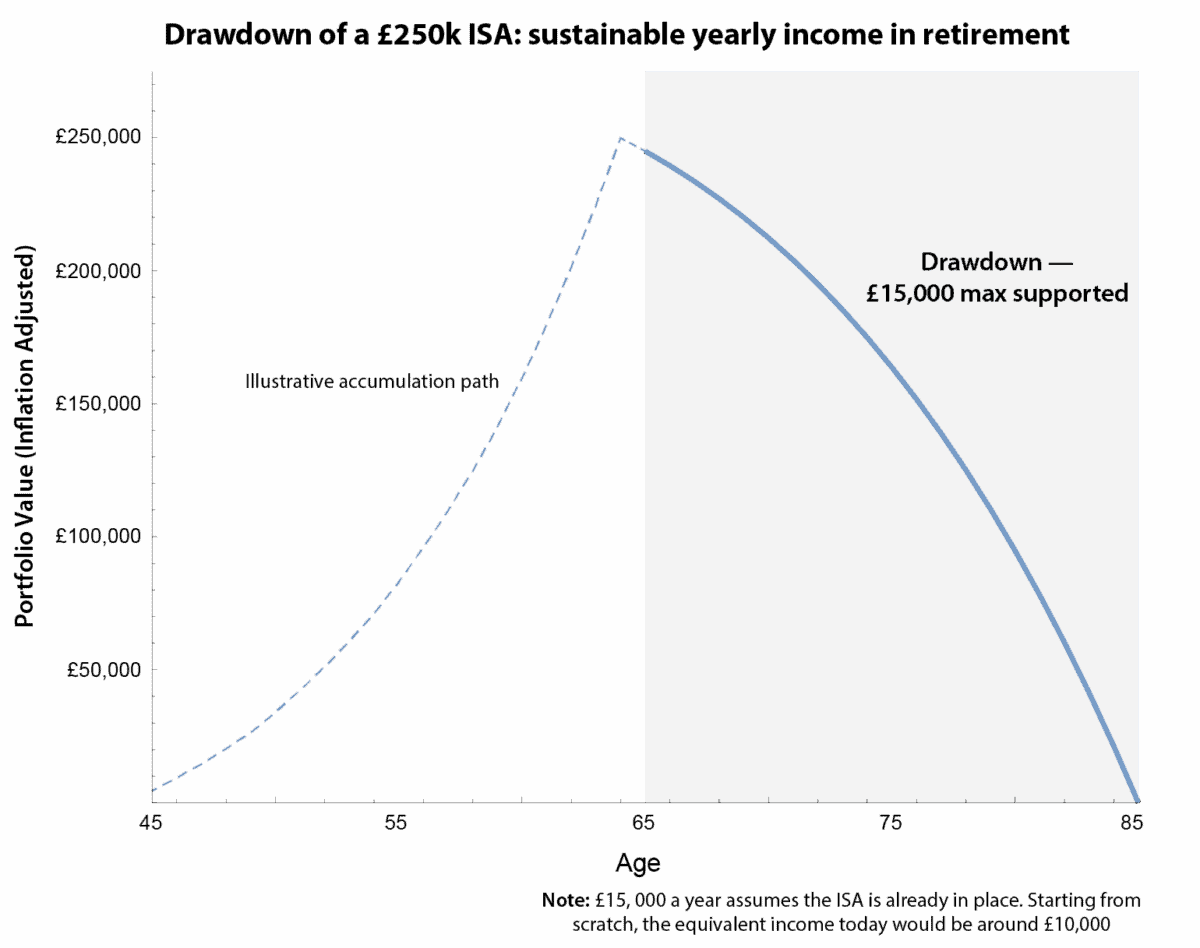

When coupled with the State Pension, £15,000 passive income – or about £1,250 a month – can make a real difference in retirement. But being in a position to withdraw that amount every year for the rest of one’s life is a different challenge.

Crunching the numbers

My calculations show that a £250,000 ISA today is the minimum portfolio needed to sustain this level of income. This assumes the portfolio grows at 4% in retirement and inflation sits at 2%. That’s money you can count on to cover spending, travel, or simply enjoy retirement with confidence.

For those starting from scratch, the income you can safely withdraw today is closer to £10,000 a year in today’s terms. The reason is simple: it’s all about when the capital is in place. More money upfront means more income immediately; building it gradually over 20 years means you also need to account for inflation along the way.

The chart illustrates this clearly. It shows the single sustainable withdrawal line for a £250,000 ISA balance. Crucially, this line doesn’t change whether the pot is already in place or you’re still building it. What changes is how that income translates into today’s spending power.

Chart generated by author

Sustainable withdrawals

The chart also tells an important story: there’s no room for overconfidence. Withdraw too much, or assume the portfolio will grow faster than is realistic, and the money could run out sooner than expected.

That is the key lesson: the line gives a baseline for planning. From there, you can adjust withdrawals to suit different phases of retirement, cope with market ups and downs, or leave a small cushion for longevity or inheritance purposes.

With careful planning, the ISA provides flexible, dependable income, letting you enjoy retirement on your own terms without complex calculations or risky assumptions.

High-income stock

If you’re thinking about generating passive income from your ISA, Legal & General (LSE: LGEN) is worth a look. The sustainability of its 8.2% dividend yield remains constantly in focus, but I think many investors miss a much bigger point.

What makes the insurer stand out is the predictability of its cash flow. The business takes in long-dated pension and annuity liabilities, invests them conservatively, and steadily returns capital to shareholders through dividends. That means the income is supported by underlying cash generation rather than short-term market moves.

For investors building a £250,000 ISA, reinvested dividends maximises compounding advantages. For those already in drawdown, those same dividends reduce the need to sell shares, smoothing withdrawals through volatile markets. In other words, the insurer’s dividends can supplement the sustainable withdrawals you plan from your ISA.

There are risks. Should high levels of inflation become the norm, that could put significant pressure on the value of its £86bn bond portfolio, thereby threatening future dividend payments.

Bottom line

Legal & General’s share price has struggled for momentum over the past couple of years. But despite this it continues to reward investors with marketing-leading returns. With an adjusted price-to-earnings (P/E) ratio of just 13, I’m very comfortable holding it in in my Stocks and Shares ISA. Indeed, I recently topped up my holdings.

This story originally appeared on Motley Fool