{kind=link}

Image source: Getty Images

Rolls-Royce (LSE:RR) has been the biggest FTSE 100 success story of the last five years. But there are a few names I’m expecting to be even better investments between now and 2030.

One is Croda International (LSE:CRDA). The company’s been under pressure since the end of the pandemic, but I think it’s in a similar position to where Rolls-Royce was five years ago.

Cyclical upswing

Things really started to take off for Rolls-Royce in the second half of 2022. And the biggest reason for this is clear – travel demand came back with a vengeance after Covid-19.

This took the firm from a downward spiral to an upward one. Higher free cash flows were used to bring down debt, which reduced interest payments, which led to higher free cash flows, and so on.

All of this however, was brought on by a sharp increase in travel demand. This was the initial catalyst that halted the company’s losses and got it back on a positive trajectory.

That’s not to underestimate the effect of an outstanding CEO, strong progress in the firm’s nuclear division, and higher defence spending. But the biggest reason has clearly been a cyclical recovery.

Cyclical downturn

Croda’s been the opposite of Rolls-Royce. The firm saw a boom in demand – especially for its lipids that were used in pharmaceuticals – during the pandemic, but this has fallen sharply.

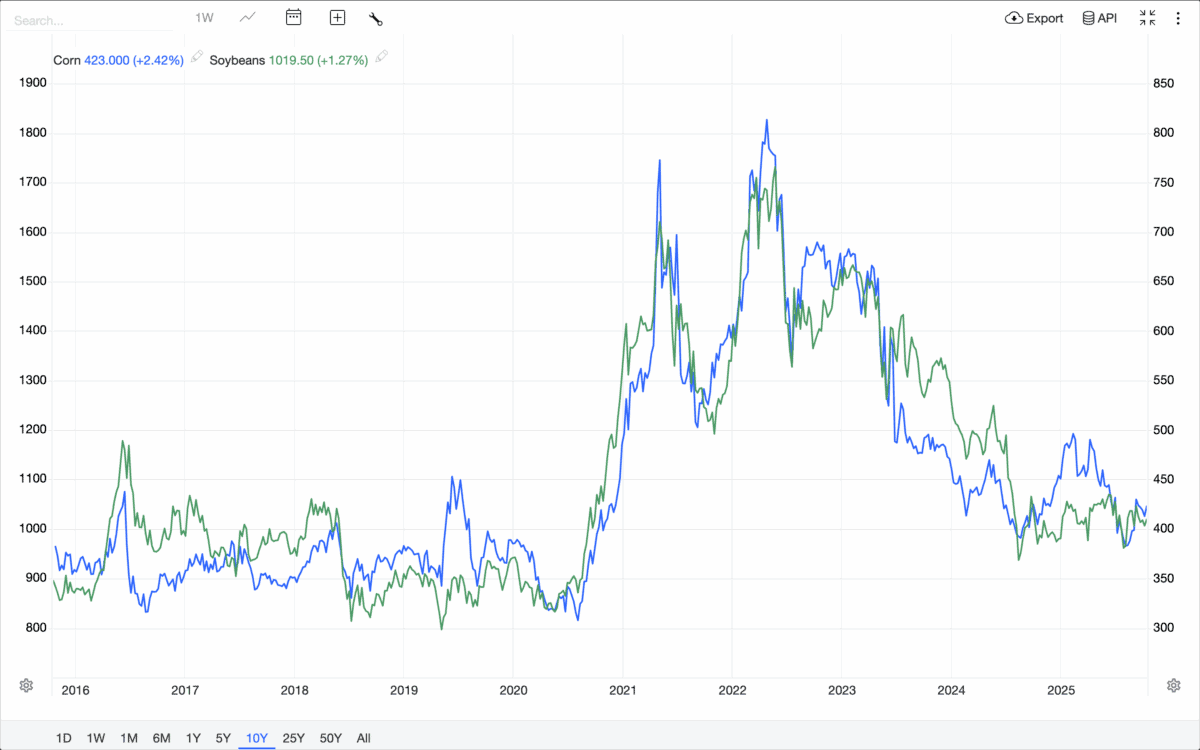

The problem however, hasn’t just been life sciences. Something similar happened in the firm’s agricultural chemicals division, as prices for corn and soybeans jumped during the pandemic.

Source: Trading Economics

This meant farmers bought more of Croda’s crop chemicals, which boosted sales. But the result has been higher inventory levels, which have caused revenues to falter in the last couple of years.

I think however, there are signs that conditions are starting to normalise. And that makes me pretty optimistic for the company going forward.

Signs of a recovery

At the end of September, Pfizer announced a deal to invest heavily in US pharmaceutical manufacturing. That should boost demand for Croda’s life sciences chemicals.

Things are also looking positive in other parts of the business. There are signs of sales growth as inventory levels start to run down in the end markets the company’s other divisions sell into.

The recent challenges have been weighing on Croda’s finances and its most recent dividend wasn’t covered by free cash flows. So the firm arguably needs the recovery I’m anticipating.

If this doesn’t come, then there could be further trouble for the stock. But it’s trading at unusually low valuation multiples, meaning the share price could go a lot higher if things go as I’m expecting.

Falling knives

With cyclical companies, the key is to buy them when they’re out of fashion. That can be in a recession for a firm like Rolls-Royce or low crop prices in the case of Croda.

Importantly though, investors need to have some sense of where they are in the cycle. The best time to consider buying is when signs of recovery are beginning to show up.

With this in mind, I like Croda much more than Rolls-Royce right now and see it as one to consider. Increased investment in US pharmaceuticals and inventories starting to run down are positive signs for the next five years.

This story originally appeared on Motley Fool