{kind=link}

Before heading out on a trip abroad, there are many things that you need to organize. You need to plan your flight, your accommodations, your transport, and how you’re going to pay for it all.

Despite the rise in credit card use and acceptance around the world, the reality is that many countries are still very reliant on cash.

With that in mind, here are five of the best ways to turn your Canadian dollars into foreign cash before or during your next trip.

>

1. Use a Prepaid Card

Sometimes it’s better to just get your cash on an as-needed basis at your destination. A prepaid card loaded with Canadian dollars can give you low-cost access to foreign ATMs without the usual markups, and several Canadian fintech products now make this remarkably painless.

Wealthsimple Prepaid Mastercard

The top option for Canadians withdrawing cash abroad is the Wealthsimple Prepaid Mastercard. This card charges no foreign exchange fees on purchases or ATM withdrawals, processing everything at the Mastercard exchange rate without the usual 2.5% markup.

What really sets it apart is that ATM fees charged by the machine itself are reimbursed by Wealthsimple. In many countries, local ATMs charge a flat fee per withdrawal, sometimes as high as $13 per transaction in countries like Thailand. With the Wealthsimple Prepaid Mastercard, those fees are refunded to your account, making it one of the cheapest ways to access cash abroad.

The card is tied directly to your chequing account within the Wealthsimple app. There’s no credit check and no revolving credit line – just a prepaid balance you control. To get started, you’ll need a Wealthsimple account and then request the card through the app.

It’s worth noting that Wealthsimple recently phased out cash back rewards on this card, so there’s no reason to use it for everyday purchases. Instead, treat it as a dedicated cash-access tool for travel, and pair it with a no-FX credit card like the Scotiabank Passport® Visa Infinite* Card for spending.

Other Prepaid Options

The Wise debit card is worth a look if you travel frequently and want to hold multiple currencies in a single account. It converts at the mid-market rate with no markup, and you get two free ATM withdrawals per month up to $350 (CAD). After that, fees of $1.50 per withdrawal and 1.75% on amounts over $350 apply. It’s a good fit for multi-currency travellers, but for pure cash access, Wealthsimple is cheaper.

The EQ Bank Card is another no-FX prepaid Mastercard that earns 0.5% cash back on all purchases. EQ Bank doesn’t charge for international ATM withdrawals on their end, though local ATM fees are not reimbursed abroad. It’s a decent all-around travel card, but again, it can’t match Wealthsimple’s global ATM fee reimbursement for cash withdrawals.

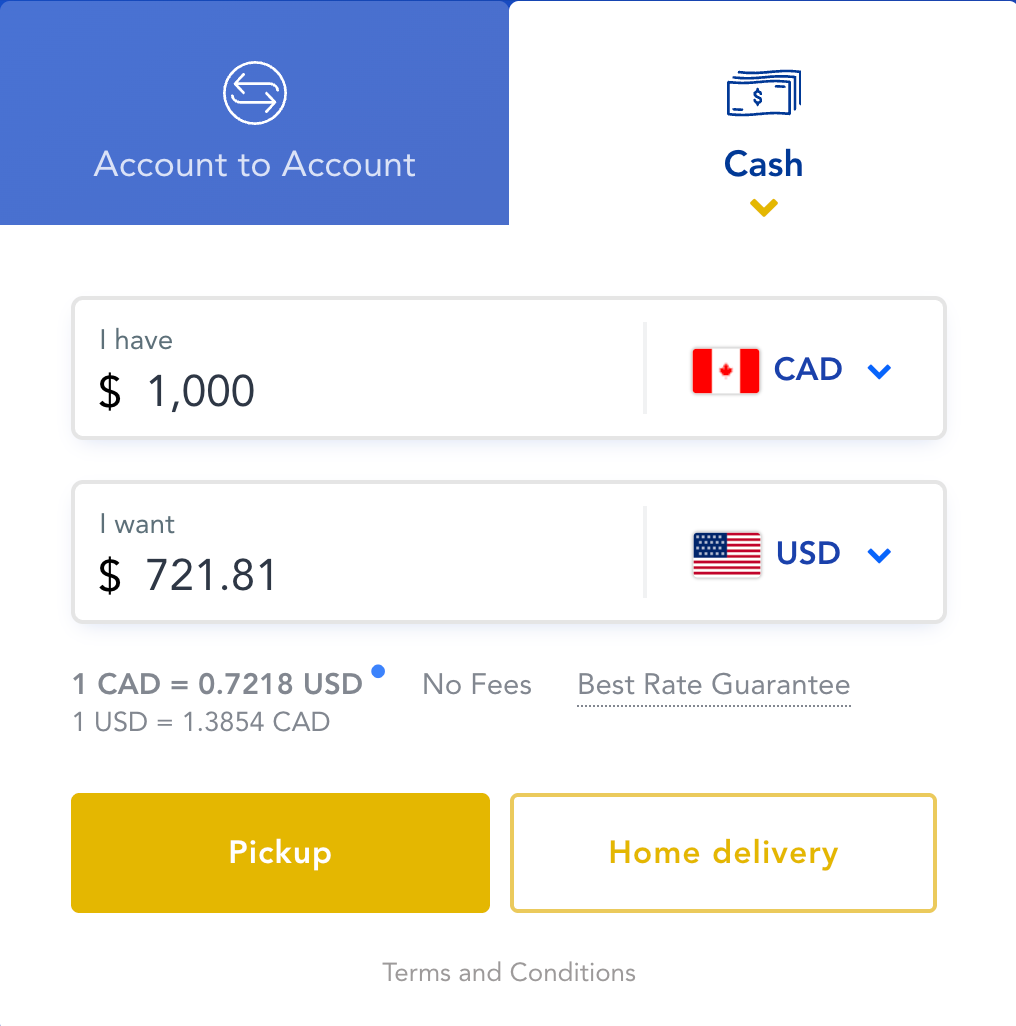

2. Order from an Online Broker

If you prefer to have physical cash in hand before you leave, you can check what foreign exchange rates are available on the open market. In this digital era, several businesses have gone online and offer home delivery.

Most of these online brokers are subject to monthly caps on the amount of cash that you can order (presumably in order to prevent money laundering or other unsavoury activity).

There are a few websites that offer this service, but by far the best rates we’ve seen thus far have come from the Toronto-based forex exchange Interchange Financial, so let’s look at what we’ll get for our CAD-to-USD example:

This is quite competitive, standing at about $11 (USD) more than what you’d typically get from a major bank. However, note that Interchange Financial will require any amount of cash you purchase to be divisible by the smallest unit of bills that they have in inventory.

This means that your purchase total will be rounded up to the nearest amount that fits within this requirement.

Interchange Financial is a solid option overall, and the free Canada-wide delivery is a nice touch.

Payment can be made via a Visa Debit card or Interac e-Transfer, and the money purchase limits are $2,500 (CAD) per month.

In case you’re feeling naturally suspicious of dealing with a private online broker, do note that Interchange is fully regulated by FINTRAC. You’ll want to ensure that you do your research on any other online broker before doing business with them.

3. Pick Up at Your Bank (or Have It Delivered)

For some folks, shipping large amounts of currency through a third-party broker sounds unappealing. In that case, your own bank may be the simplest option. Most of the Big 5 banks in Canada will have US dollars in stock at your local branch, and they’ll often have euros and pounds sterling as well.

The exchange rates at major banks tend to sit about 1.5–2.5% above the mid-market rate, so you won’t get the best deal compared to a dedicated broker. However, the convenience and peace of mind of working with your existing bank can be worth the tradeoff.

CIBC stands out here. You can order foreign cash in up to 65 currencies through CIBC Online Banking or the mobile app, with three free delivery options: any CIBC banking centre, your home address, or Toronto Pearson Airport. The exchange rate locks in at the time of your order, and there are no additional ordering fees. You’ll need a CIBC chequing, savings, or personal line of credit account.

RBC also offers online ordering in over 40 currencies, with pickup at any of their 1,200+ branches across Canada. Daily ordering limits are $2,500 for personal banking clients and $5,000 for business clients, with orders typically ready within three business days. No additional fees are charged beyond the exchange rate.

TD lets you order through EasyWeb for branch pickup within three to seven business days. The rate is locked in at the time of purchase. You can also withdraw up to $1,200 (USD) directly from TD ATMs, which can be handy if you just need a smaller amount of US cash quickly.

If you bank with BMO or Scotiabank, foreign exchange is still available but typically requires an in-branch visit rather than online ordering.

Overall, CIBC’s free home delivery option makes it the strongest bank-based choice for getting foreign cash. For everyone else, placing an order through your bank’s online banking and picking it up at a nearby branch remains a reliable fallback.

4. Western Union Remittances

Another option to consider if you’re heading to smaller locales where ATMS and money changers are limited (or non-existent), or to a place like Argentina with its Blue Dollar rate, is to send yourself money using Western Union.

When you send yourself money through this process, it can then be picked up at your convenience at any Western Union branch you designate. You should keep in mind that although the amount you remit never expires, it does need to be renewed if it’s not picked up within 90 days.

Sending money through Western Union can be incredibly useful if you’re planning to spend a long period of time in an off-the-beaten path location with no ATMs and where locals already utilize Western Union regularly as a money transfer.

Additionally, for countries like Argentina, which has two exchange rates, Western Union lets you take advantage of the considerably better Blue Dollar rate when sending money, which saves you trying to exchange money in-country (likely at a notably worse exchange rate).

When sending money via Western Union, you may have to pay a fee of up to $7.50 (CAD) depending on how you pay for the funds to be sent. Notably, unlike most of the above options, Western Union does let you pay using a credit card; however, this will likely incur a cash advance fee from your credit card issuer.

5. Fall Back on Your Debit Card

When all else fails, your regular debit card will still work at most international ATMs. As long as you’re using a machine at a reputable bank, the spot conversion rate will generally beat local currency dealers, even after factoring in the foreign ATM fee.

Those fees aren’t always unavoidable, either. Scotiabank, for example, has a significant presence in Latin America and the Caribbean, along with reciprocal agreements that let you use partner ATMs without extra charges. The other Big 5 banks have similar arrangements with international institutions.

If you’d rather not carry large amounts of cash, withdrawing what you need at your destination is a perfectly reasonable approach.

Conclusion

Figuring out how to pay for things abroad doesn’t have to be stressful. Whether you’re loading up a prepaid card, ordering cash from a broker, or just hitting an ATM at your destination, there are plenty of ways to avoid overpaying on exchange rates.

If I had to pick one setup for most trips, it would be a Wealthsimple Prepaid Mastercard for ATM withdrawals paired with a no-FX credit card for purchases. That combination covers the vast majority of situations, and you won’t lose a cent to markups or ATM fees.

This story originally appeared on princeoftravel