{kind=link}

Image source: Getty Images

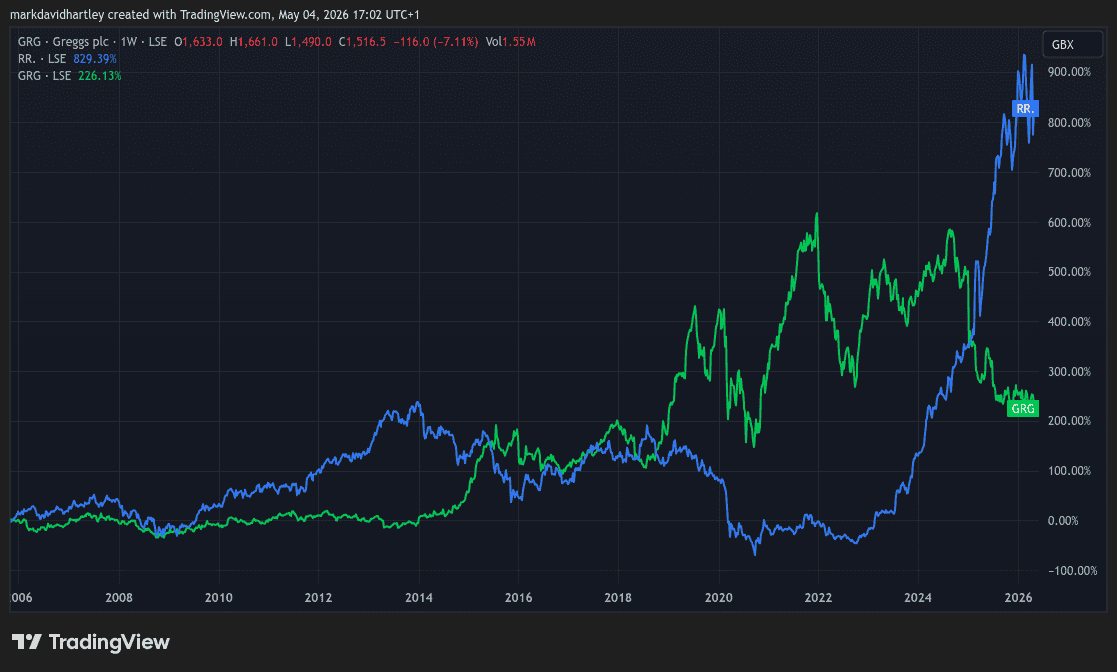

Currently trading around £15 each, Greggs (LSE: GRG) shares have lost more than half their value since their 2022 high above £33.

It’s a shocking comparison to the promising growth stock it once was in the late 20-teens. And that’s exactly why it closely mirrors the price activity of Rolls-Royce between 2010 and 2020.

So could Greggs do a full 180 and rack up exponential gains in the coming five years?

Let’s take a closer look.

Macro challenges

The parallels between Greggs today and Rolls-Royce in prior years run deeper than just the share price.

In both cases, sharp downturns were driven largely by external factors. In Rolls’ case, the Covid-19 pandemic grounded global air travel. For Greggs, shifting consumer habits and wage hikes have hit profits hard.

But we can’t attribute Rolls’ success purely to recovering air travel, otherwise all airlines would have similar fortunes. The role of CEO Tufan Erginbilgiç in the recovery can’t be overstated, which is where Greggs comes into question.

Can Gregg’s CEO Roisin Currie, appointed in 2022, help the bakery enact a Rolls-like recovery?

Why a Greggs recovery is plausible

Several factors play into the narrative of a strong recovery for Greggs. Most notably, it still has a strong underlying brand and cash flow.

It’s viewed as a leading ‘value food‑to‑go’ brand, with resilient like‑for‑like sales, and a pipeline of store openings and new‑venue formats (rail, forecourts, supermarkets).

After its sharp fall from 2021 highs, analysts now describe it as ‘cheap’ relative to earnings and cash generation. The current price is only 12 times estimated future earnings.

That’s attractive for a consumer‑defensive, asset‑light business. With costs falling, management now targets a return on capital employed (ROCE) recovery of around 20%. So even a modest margin improvement could re‑rate the shares.

That means the growth narrative of the 20-teens could return in full force – if external issues ease.

But will it be a Rolls-like recovery?

While I’m optimistic about Greggs, I’m also realistic. Rolls’ 1,000%+ rally came from a leveraged balance sheet turnaround, double‑digit margin expansion, and extensive government defence spending.

Greggs is different in that it’s a smaller, more cyclical, competitive consumer‑retail stock. It doesn’t exhibit quite the same structural leverage and explosive potential.

Add to that ongoing challenges like the cost-of-living crisis, weather-sensitive foot traffic, and evolving eating habits, and it faces a tough future.

I think it’s reasonable to expect growth in the 300%-400% range over the coming five years if conditions improve and it caters to changing habits.

But it’s highly unlikely that any FTSE stock will match Rolls’ once-in-a-decade performance.

The bottom line

Arguably the UK’s most popular high street bakery chain, Gregg’s has grown aggressively since 2020. Between 2020 and 2025, it increased its store count from around 2,000 to over 2,700.

But the rapid expansion may have been premature. After the Labour government introduced budgetary changes in October 2024, the company was faced with the threat of rising costs.

And yet despite these ongoing risks, it’s managed to maintain a healthy balance sheet. Shrinking margins are a concern but growing cash flow and an attractive valuation hint at recovery potential.

The future may be uncertain, but for value investors optimistic about the UK economy, Greggs is a compelling option to consider.

This story originally appeared on Motley Fool